6 steps to inventory reconciliation and why it’s important for your business

In today’s fast-moving retail world, taking the time to conduct an inventory reconciliation can be difficult. It means pulling people away from their day-to-day tasks and doing what may seem like mundane (and routine) work. However, maintaining accurate inventory is crucial to business success.

Just ask these folks about the importance of tight inventory controls. Target, for example, found that barcodes of Barbie products didn’t match the numbers in their computer system. These mismatched product counts led to empty store shelves and disappointed shoppers. It also led to a $2 billion loss. Nike executives counted $100 million in sales due to inventory tracking issues. Ralph Lauren saw their profits drop 50% over two years because itself-admittedly couldn’t get a handle on its inventory management.

It can happen to the largest, most sophisticated companies and it happens to small and medium-sized businesses all over the world. If you’re in the retail business, your inventory is constantly changing. There are so many moving parts across locations and platforms that things can sometimes get out of sync.

Making sure your actual inventory aligns exactly with your inventory records is crucial. That’s where inventory reconciliation comes into play.

What is inventory reconciliation?

Inventory reconciliation is the act of taking inventory of everything you have and making sure your stock records match reality. It’s important to reconcile your inventory periodically to find any discrepancies that need to be addressed.

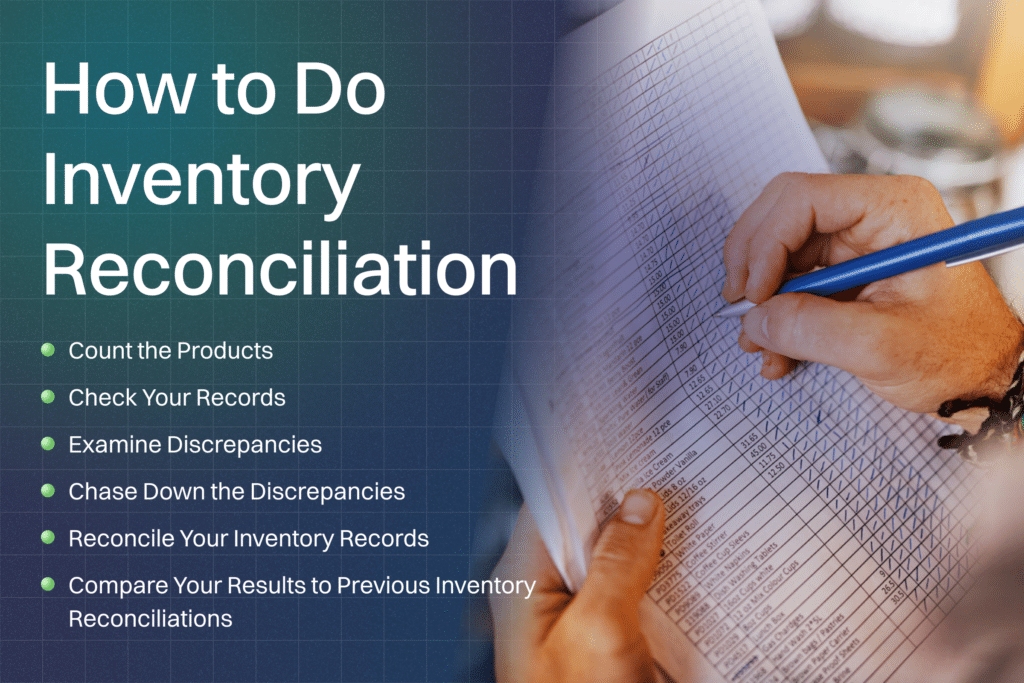

How to do inventory reconciliation

Our implementation experts at Linnworks recommend a 6-step process many businesses use when conducting inventory reconciliation. It starts with the count.

1. Count the products

Count the products on hand and compare the inventory records with the physical inventory. Most companies do multiple counts to reduce errors.

This includes noting stock numbers and serial numbers to match up with the records.

How you conduct your physical inventory can vary. Here are the common methodologies: full inventory or cycle counting.

- Full count inventory

Using the full inventory count method, your team or an outside inventory company will come into your facility and count every physical item. They can track these counts with pencil and paper or barcode scanners or RFID technology.

No matter what method they employ, they will physically count every item in your inventory all in one time period.

The upside of this approach is that it provides an accurate, up-to-the-minute accounting of all stock items.

The downside is that this kind of count often requires shutting down operations while conducted. Depending on the size of your warehouse and stock areas, a full physical count could cost you money as you shut down for a day or more.

Beyond that, one giant physical inventory can be a daunting task. The sheer volume of the undertaking can lead to errors in counts.

- Cycle counts

If you conduct cycle counts for your inventory tracking needs, you’ll find counts are easier and less stressful to perform.

In cycle counts, your employees will count specific items or areas of your inventory daily. Over time, you’ll count your entire inventory, only in pieces.

The upside here is that cycle counts can be conducted without disrupting the daily operation of your business. The smaller counts are less stressful, and because they cover only a portion of your warehouse, there’s less chance of error.

The potential downside to this method is that it relies on data collected over time. The physical inventory is very up-to-date because it’s all conducted in one session. Cycle counts spread out over time, so there can be discrepancies as time passes.

To alleviate this, for important counts where accuracy is paramount, companies will run their cycle counts but still conduct a full inventory occasionally to ensure accurate numbers.

No matter which method you choose, the first step in any reconciliation is knowing the amount of product you physically have on hand. Counting will provide this data.

2. Check your records

Make sure that your inventory records, including inventory control systems, are current. This includes accurate and up-to-date sales and invoices.

Compare the inventory records with each item listed in stock. Make sure any stock numbers and serial numbers are accurate. Items that do not have any serial numbers or stock numbers associated with them should be compared to inventory-on-hand numbers and supplier invoices.

Like in the counting process, most companies will check and re-check the record matching to verify accuracy.

Here are some common issues to look for while checking records:

- Missing or misplaced paperwork

One of the most common causes of inventory discrepancies in the reconciliation process is missing paperwork. Inventory-related paperwork should be filed and kept in one accessible location. Inventory management software can make this process easier to manage.

- Human error

Mistakes happen, and this is particularly true when it comes to tracking inventory. If there’s a discrepancy, make sure you re-check the count and look for places where an employee might have made a mistake.

- Math errors

One of the most common types of human error involves math. If you find a problem when reconciling counts with inventory numbers, save yourself time and headache by checking the math first.

- Unlisted Items

This one is largely self-explanatory. Sometimes inventory will wind up in your warehouse without being adequately checked in. If you find unlisted items during your count, it’s important to research them (by finding paperwork if possible) and then add them to your inventory for future counts.

- Supplier Fraud

Unfortunately, supplier fraud is a rare but real issue. This is why accurate inventory receiving practices are so important. It’s easier to catch supplier fraud early than it is during a reconciliation.

- Backflushing

If you’re using a perpetual inventory approach, you’re probably using the practice of backflushing as part of your accounting. Here’s an official definition of what the practice entails:

“Backflushing is automatic accounting of material consumed for production, at the time of confirmation of the production, e.g. when a 4-wheeler automobile is rolled out from assembly line, 4 wheels and tires are deemed to be consumed and issued to production order automatically by way of backflushing by the system.”

If you use backflushing in your business, you’ll want to account for the practice during your inventory reconciliation.

- Shrink

No one likes to think about shrink, but it’s a genuine issue that affects every business. If numbers are off and the previous steps haven’t helped you find a solution, you may have a shrink problem.

Whether it’s customers or employees taking items, you’ll want to get a handle on these issues ASAP.

3. Examine discrepancies

As you compare the results of your inventory audit, you will likely uncover discrepancies. Once the audit is complete, it’s time to address these discrepancies.

Some discrepancies may be attributed to human errors or math errors. If it appears that’s not the case, the next step is going through sales records to identify the possibility that sales had not been recorded accurately. If you cannot find missing sales receipts, you may have lost or misplaced merchandise or indications of theft or fraud.

4. Chase down the discrepancies

It’s up to you to determine the acceptable level of shrinkage in your business. If the number or value of missing merchandise is small, it may be more time-consuming and expensive to narrow down the cause of the loss rather than move on. If you decide to track it down, look first at your systems and then at your employees.

Often, steps get missed in the recording process either in the warehouse, the retail floor, or the eCommerce platforms. It’s helpful to interview employees responsible for each step to determine if there’s an explanation for the discrepancy that can be addressed.

The key consideration here involves determining whether the discrepancy is big enough to warrant resolving. Sometimes you’ll have to “pick your battles” in terms of resolving discrepancies. Low-value items might not be worth the time and energy expenditure, for example.

Other times, there may not be an answer for the discrepancy. This requires accepting that a mistake has occurred but not knowing what it is because you don’t have the information to resolve it.

You’ll always want to resolve as many discrepancies as you can. Still, it’s important not to become so bogged down with the resolution process that you stretch out the reconciliation process to the next inventory count.

5. Reconcile your inventory records

Whether you can track down the discrepancy or not, you must have an accurate inventory count. Adjust your record to match the physical count. Then, make a note of the changes for updated financial reporting or write-offs.

It’s important to remember that while you should strive to resolve all discrepancies, there comes the point where you’ll need to accept that some issues can’t be explained simply. When you reach this point, it’s time to reconcile and move forward. Just don’t forget about the discrepancies because they’ll be an essential component of our next step and future reconciliations.

6. Compare your results to previous inventory reconciliations

As a final step, compare the results of your inventory reconciliation with previous ones. This can help surface trends and patterns and indicate areas for further examination.

This is especially useful if you have unresolved discrepancies. Being aware of these unexplained issues allows you to better focus on those particular items, which will either prevent future issues or help you discover what the problem is (shrink, human error, and so on).

Why is inventory reconciliation important?

When the records don’t agree with the physical inventory, there’s an issue.

Even with the right inventory management and control software, there’s always a bit of shrinkage in inventory. According to the National Retail Federation, the average shrink rate (as a percentage of sales) is 1.38% for U.S. retailers. While that may seem like a small percentage, it adds up to just shy of $50 billion of inventory that’s unaccounted for.

There’s no doubt that some of this shrinking is caused by human error and mistakes. The information in the inventory control system is only as good as the data that’s entered and managed. Inventory reconciliation helps you monitor the shrinkage and look for the warning signs of bigger issues, such as customer or employee theft.

Shoplifting and customer theft make up 36% of inventory losses while employee theft accounts for 30%. When the inventory numbers don’t match up with the physical inventory or your shrinkage rates start to grow, it may be a signal that you need to improve your loss prevention strategies. It can also reveal systematic problems, such as missing shipments or even fraud by suppliers.

Shrinkage is just one of the inventory KPIs you need to track using inventory management software.

Streamlining inventory reconciliation

Inventory reconciliation can be a tedious and time-consuming task. For retailers, it can mean after-hours counting or even shutting down operations for a few days to do manual inventory checks. This may not be an option for you.

Some companies will streamline the reconciliation with a process called “cycle counting.” Instead of a once-a-year reconciliation process, they have their counting broken down so that some inventory items are being counted all the time. Doing a little bit at a time may be easier than doing it all at once.

Another way to handle inventory reconciliation is to break it down by priorities. Instead of counting everything, you group products into categories and focus more heavily on high-value items. They use what’s known as the ABC Inventory Control System.

The ABC inventory control system

Rather than look at all inventory equally, it’s first divided into three categories:

- Category A: High-value inventory

- Category B: Moderate-value inventory

- Category C: Low-value inventory

In most companies, Category A (high-value inventory) will represent 15-25% of items but represent large volumes of sales and/or profitability. Inventory that is less critical to your operation is grouped into Categories B or C depending on their value.

Category A inventory should be counted more frequently as it has a greater impact on your operations. Shrinkage or loss is a much bigger concern than for lower value items and it’s more important to identify problems or missing stock more quickly.

Delivering more accurate inventory management

If you find some discrepancies as you are conducting your inventory reconciliation, don’t despair. It’s a normal occurrence. The larger the enterprise, the more likely you’ll find something’s not quite right. It’s when the numbers grow out of proportion, or you spot troubling trends, that you’ve got a problem.

The best way to keep accurate and current accounts of your inventory is to utilize an end-to-end inventory control system that ties your POS system, warehousing, and delivery together in an integrated manner. This allows for greater accuracy and accountability while providing real-time records for review.

Interested in learning more? Here are a few more resources we think you’ll like!

Ready to improve your inventory reconciliation? One of our knowledgeable sales consultants is ready to walk you through exactly how SkuVault Core can benefit your business and answer all your questions about how our powerful Inventory and Warehouse Management System can help address the needs of your unique business.